2025 was the reset. 2026 is the monetization year. We shut down what was not working, preserved the assets that matter, restored the public-company platform, and are now focused on converting users, fans, creators, advertisers, sports audiences and financial-services customers into revenue.

Los Angeles, June 29, 2026 (GLOBE NEWSWIRE) — Triller Group Inc. (Nasdaq: ILLR / ILLRW) (the “Company” or “Triller”) – is pleased to provide the following responses to questions submitted by shareholders in connection with the Annual General Meeting of Shareholders held on June 10, 2026 (the “Annual Meeting”). The Company is committed to transparency and open communication with its shareholders and appreciates the engagement of those who submitted questions.

AGM Outcomes

At the Annual Meeting on June 10, 2026, shareholders approved the principal proposals put forward by the Board, including:

– Change of the Company’s name from Triller Group Inc. to Eight Holdings Inc.

– Authorization for a reverse stock split at a ratio of no more than 1-for-10 within one year

– Adoption of the 2026 Equity Incentive Plan

– Nasdaq 20% issuance approval (flexibility for private placements exceeding 20% of outstanding shares)

These approvals provide important governance and capital-markets tools.

The Q&A below addresses the key questions raised at and around the meeting and explains how management intends to use these tools in a disciplined, value-focused manner.

Shareholder Q&A

1. Why are we publishing these answers now?

At the Annual Meeting, shareholders asked direct questions about the reset, the legacy Triller app, Project Eight, share price, valuation, capital raising flexibility, leadership stability, and the path to monetization. We committed to provide written answers publicly, and this document is intended to follow through on that commitment.

The purpose of this document is to give shareholders a clearer explanation of the strategy, the decisions already taken, and the principles that will guide management going forward.

Bottom line: We heard the questions, and we are answering them directly.

2. What is the right way to understand 2025 and the Company’s current position?

The right way to understand the Company today is simple: 2025 was the reset; 2026 is the monetization year.

In 2025, management focused on stabilizing reporting, restoring public-company discipline, rationalizing legacy operations that did not have acceptable economics, preserving the assets that matter, and preparing the business for a revenue-first operating model.

The Company also fought its way back to Nasdaq. Public materials describe 107 days off Nasdaq, five delinquent filings resolved, and more than $12 million invested in the compliance rebuild, including systems, audit and governance work.

The reset was difficult, but it created the conditions for the next phase of execution and monetization.

Bottom line: The reset cleared the path; the story now is execution.

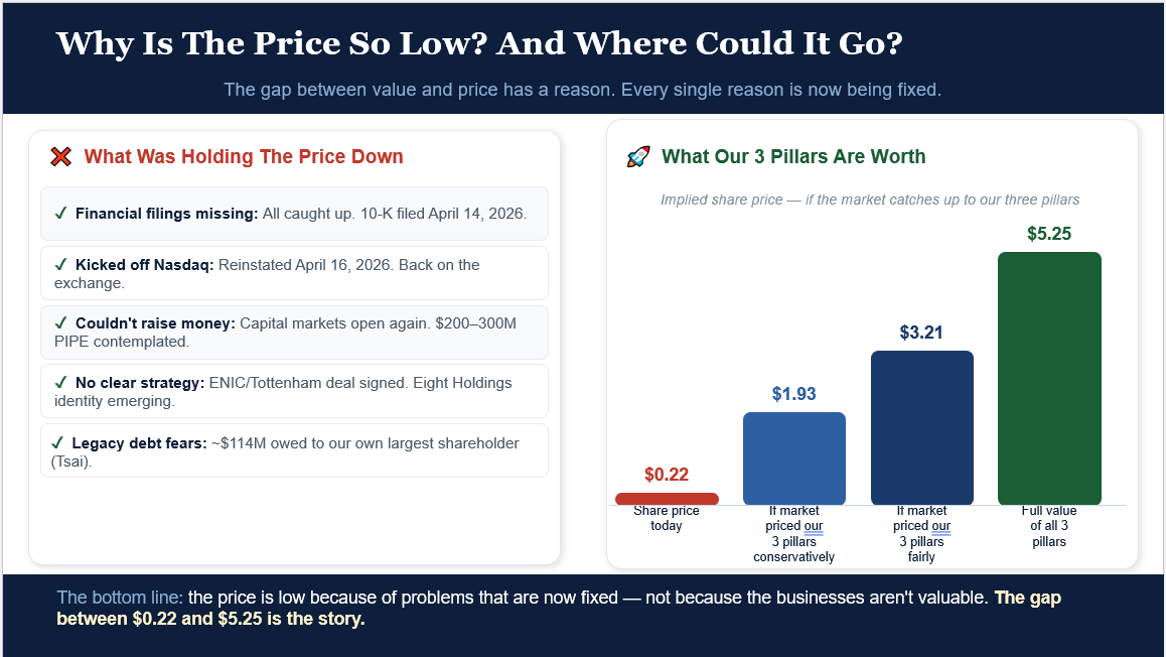

3. Why is the share price so low?

We understand the frustration. We addressed this directly at the Annual Meeting by showing an illustrative sum-of-the-parts framework. The purpose was not to give a price target or investment recommendation. It was to explain why management believes there is a large gap between the current trading value of the Company and the value of the assets and operating platforms inside the Group.

In management’s view, the share price has been weighed down by several legacy issues: prior financial reporting delinquency; the Nasdaq suspension and reinstatement process; uncertainty around capital access; no clear strategic narrative during the reset period; Yorkville-related concerns; legacy liabilities and balance-sheet concerns; zero reported 2025 revenue from the social media and sports streaming segments; dilution concerns; and uncertainty around execution of the new business plan.

These concerns are understandable. Shareholders lived through a difficult period. But many of the issues that created the discount have either been fixed or are actively being addressed. The Company is current in its filings, Nasdaq trading resumed on April 16, 2026, the public-company platform has been restored, management has clarified the strategic direction, and the Company is now focused on revenue, capital discipline, and execution. What remains is for the Company to generate revenue and for the market to re-rate the Company as measurable operating progress is delivered.

At the AGM, management showed a simple framework: the Company should be understood through three operating pillars – Social Media, Eight Sports Capital, and Financial Services / AGBA. The slides showed management’s illustrative view that those pillars together represent value materially above the then-current market capitalization. That analysis was intended to show the magnitude of the possible disconnect, not to predict a trading price.

The reason the share price is low, in our view, is that the market is still pricing the old Triller story: filing issues, Nasdaq pressure, legacy liabilities, no social media revenue, BKFC deconsolidation, and uncertainty around capital needs. The story management is trying to build is different: filings are current and AGBA remains a real revenue anchor, Project Eight or alternative social monetization pathways can activate legacy scale, Julius can improve commercial intelligence, sports assets can become monetization infrastructure, and Triller Sweeps and other partner-led models can add additional revenue paths.

That said, we are not asking investors to rely on valuation slides alone. The market will decide the share price. Our job is to execute. Shareholders should judge us by measurable progress: monetized users, completed ad views, revenue per engaged user, customer acquisition cost, brand rebooking, sports monetization, AGBA revenue and productivity, operating-expense discipline, and progress toward breakeven.

Bottom line: We believe that the share price reflects the market’s still applying a legacy discount to the Company. Management’s responsibility is to earn that discount back through execution, disciplined capital allocation, transparent reporting, and measurable operating results.

4. Why did management shut down the legacy Triller app? Is the Company killing the business?

No. Management shut down the legacy app because continuing to fund a product without a sustainable revenue model would have destroyed shareholder value.

The legacy app had real cultural relevance, especially in music, dance and creator culture. But cultural relevance is not the same as a scalable revenue model. Management chose not to keep funding spend that did not produce acceptable economics.

The scarce assets were preserved: the historical user base, cultural relevance, creator history, brand equity where it still converts, and the public-company platform. The plan is to rebuild around potential monetization rather than nostalgia.

The strategy is not to recreate old Triller. The strategy is to build Eight around monetization: social and creator monetization, sports and live-event monetization, and financial-services infrastructure.

Bottom line: We stopped what was not working, preserved what matters, and rebuilt around revenue.

5. What is Project Eight, and is the Company dependent on it?

Project Eight is the Company’s current preferred pathway to add social engagement and monetization infrastructure. It is intended to help activate the legacy Triller user base with a stronger monetization model.

However, Project Eight is not a single point of failure. Management evaluated multiple platform alternatives and selected Project Eight as the preferred path based on product readiness, monetization model, team, and speed.

The important point is that app technology is not the scarce asset. Users, distribution, cultural relevance, capital-markets flexibility, sports audiences and financial infrastructure are the scarce assets. There are many short-form video and social-video technologies in the market; far fewer have scale, culture, distribution, and public-company execution capability.

If Project Eight does not close on acceptable terms, the Company retains alternative acquisition, partnership, licensing and integration pathways. The strategic objective remains unchanged: convert existing scale into recurring revenue.

Bottom line: Project Eight is a preferred accelerator, not a dependency.

6. Why did shareholders approve a capital raising resolution? Is a financing already decided?

The capital raising resolution gives the Company the flexibility to raise equity efficiently when the right opportunity arises. Shareholders authorized a private placement of up to approximately $300 million under Nasdaq Rule 5635(d). That authorization is a tool the Company can use; as of the date of this release no definitive financing agreement has been entered into, and the timing, final terms, investors and use of proceeds of any placement remain to be determined.

The proxy statement explained that the Nasdaq 20% proposal was intended to give the Company flexibility to issue shares, or securities convertible into or exercisable for shares, in one or more private placements if the issuance exceeds 20% of outstanding common stock. The proxy also stated that no definitive financing agreement had been entered into and that terms, timing, investors and allocation of proceeds remained undetermined.

We asked for this flexibility now because the Company is considering several excellent value-adding proposals. Those opportunities may require speed, certainty and capital-markets flexibility. Pre-approval helps avoid being forced into slow, reactive or inferior financing structures later.

Any financing may be dilutive. That is why the standard must be clear: capital should be raised only when management and the Board believe the expected strategic value outweighs the dilution.

Bottom line: Shareholders have authorized the Company to raise up to approximately $300 million in equity when conditions are right; no financing has yet been finalized.

7. Will there be hidden dilution, toxic equity lines or structures like prior financings?

Management takes dilution seriously because management, directors and major shareholders are economically aligned with shareholders.

The Company does not view its shares as cheap currency. If capital is raised, it should be for value-creating purposes: completing Project Eight, recovering and properly funding BKFC, accelerating AGBA, acquiring or merging with attractive technology/assets, or structuring transactions that increase ownership, control, revenue and long-term value.

Management’s position is clear: no hidden dilution, no toxic equity-line structures, no variable-price reset mechanics, and no undisclosed conversion features designed to transfer value away from shareholders.

The Company has an experienced internal team with deep investment banking, M&A, financial-services, capital-markets and structuring experience. The team understands financing terms, control protections and dilution math.

Bottom line: Capital for compounding value is the standard; undisciplined dilution is not.

8. Why did the Company ask for reverse split authorization?

On June 25, 2026, the Company effected a reverse stock split at a ratio of 1-for-10, pursuant to the authorization granted by shareholders at the Annual General Meeting. The Board determined the final ratio in its discretion, consistent with the proxy statement disclosure that the ratio would be no greater than 1-for-10 and would be implemented within one year of shareholder approval.

The purpose of the reverse split was to support the Company’s continued Nasdaq listing requirements and to make the stock more accessible and attractive to a broader range of institutional and other investors.

Bottom line: The reverse split authorization is a flexibility tool, not the business strategy.

9. Why change the corporate name to Eight Holdings Inc.? What happens to the Triller brand?

At the Annual General Meeting, shareholders approved changing the Company’s name from Triller Group Inc. to Eight Holdings Inc. The Board determined that the name change better reflects the Company’s evolving business strategy and corporate identity, and the Company is proceeding with implementation subject to customary regulatory processes. The effective date will be communicated once confirmed.

The Triller name carries real history and cultural value, especially in music, dance, and creator culture. At the same time, the parent company requires a cleaner corporate identity that reflects the new architecture: social monetization, sports, creator tools, financial services, payments, and operating discipline. The Triller brand may still be used selectively where it supports monetization and conversion — such as certain consumer-facing initiatives. The goal is not to discard useful brand equity; the goal is to ensure the old brand no longer defines the whole company.

The name change to Eight Holdings Inc. reflects where the Company is going, not a single transaction or outcome. The Company’s strategic objective remains unchanged regardless of how individual transactions develop: convert existing audience scale into recurring revenue through a monetization-first, disciplined operating architecture.

As of the date hereof, the Company has not yet officially effected this name change.

Bottom line: The Triller brand remains a selective monetization asset where it still works. Eight Holdings is the corporate identity for the next phase.

10. Do you have the right people managing and building these businesses?

The operating model is franchise-led under Group oversight. Group leadership is responsible for capital allocation, governance, public-company discipline, financing and strategic integration. The operating franchises are led by domain experts.

This matters because the Company is not asking one centralized team to run social media, sports, financial services and creator monetization from the center. The intended model is to put specialist operators over each franchise, with Group leadership allocating capital and integrating the ecosystem.

Management has also been clear that the Company is pursuing a capital-efficient, monetization-first strategy. The Board is willing to reassess even high-profile plans when they do not match the Company’s capital priorities and execution roadmap.

The Board also has a majority of independent directors and standing audit, remuneration, and nominating/governance committees.

Bottom line: This is a global platform with franchise-level execution and Group-level capital discipline.

11. What is AGBA’s role in the new company?

AGBA is the current operating anchor and financial-services foundation of the Group. It generated the Company’s 2025 revenue and provided the commercial base while the broader reset was completed.

AGBA matters for two reasons. First, it is a real operating business with customers, product-provider relationships, regulatory infrastructure and a long operating history. Second, it can provide financial-services infrastructure, payment rails, customer access and operating discipline to the broader Eight ecosystem.

The strategy is not to treat AGBA as a disconnected legacy asset. The strategy is to use AGBA as the financial-services and operating infrastructure layer that supports broader monetization across the Group.

Bottom line: AGBA gives the Group operating ballast and financial infrastructure while the higher-growth engines are activated.

12. What should shareholders track next?

Management intends to be KPI-driven. The Company’s goal is to provide data that helps investors judge whether the plan is working.

- For social / Project Eight or alternatives: ad-engaged users, completed ad views, revenue per engaged user, customer acquisition cost, retention, creator activity and brand rebooking.

- For sports: events, media-rights revenue, sponsorship revenue, app revenue, fan conversion, and control/ownership progress where applicable.

- For AGBA: revenue, consultant count, consultant productivity, gross margin, operating expense and pre-tax profit.

- For the Group: cash use, financing discipline, reporting discipline and progress toward monetization milestones.

Management intends to provide updates against these and other relevant operating metrics as the businesses scale.

Bottom line: The next phase of communication should be more data-driven, not more promotional.

13. What is management’s closing message to shareholders?

The old story was Triller: a culturally relevant platform with too much burn and not enough revenue. The new story is Eight: a monetization-first platform built to convert users, creators, fans, advertisers and financial-services customers into revenue.

The Company inherited difficult issues. Management chose to face them directly. The Company is now focused on disciplined execution, prudent capital allocation, governance, and rebuilding shareholder value.

The priority is simple: revenue first, scale second, optionality third.

Bottom line: We are building a clearer, more monetizable and more disciplined company.

Appendix A: Valuation Slides Shown at the Annual Meeting

The following two slides were shown on screen at the Annual Meeting. They are reproduced here so that the written Q&A release reflects the materials shareholders saw at the meeting.

The slides are illustrative only. They reflect management’s discussion framework at the meeting and should not be treated as valuations, appraisals, forecasts, investment advice or price targets. Investors should review the Company’s SEC filings and consult their own advisors before making any investment decision.

The slides are reproduced for fairness of disclosure because they were shown at the Annual Meeting; they have not been updated to reflect events after the meeting.

Valuation Slide 1 – Revised Presentation Slides

Valuation Slide 2 – Shown at AGM

The foregoing slides represent management’s current estimates as to potential valuation. There can be no assurances as to when or whether such objectives will be achieved.

About Triller Group Inc.

Triller Group Inc. (Nasdaq: ILLR; ILLRW) is a technology and media company operating Triller App, a social media and live-streaming platform focused on music, sports, fashion and culture, together with AGBA Group, a Hong Kong-based financial-services and platform business with longstanding operations in wealth distribution, healthcare and related services across Asia.

Safe Harbor Statement

This press release contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995, including statements regarding resumption of trading on Nasdaq, estimates as to potential valuation, the Company’s ability to maintain timely SEC periodic reporting and Nasdaq compliance, the effectiveness of its remediation measures, the anticipated benefits of resumed Nasdaq trading, and the timing of future corporate updates. These statements are based on Triller’s current expectations and assumptions and involve risks and uncertainties that could cause actual results to differ materially, including risks relating to the effects of the period of trading suspension and resumption of trading on Nasdaq, market conditions, the Company’s ability to execute its monetization and operating plans, the availability of financing, the identification, negotiation or completion of any acquisitions or other strategic transactions, compliance with listing standards and reporting requirements, legal or regulatory proceedings, and the other risks described in Triller’s SEC filings. The words “believe,” “estimate,” “anticipate,” “project,” “intend,” “expect,” “plan,” “outlook,” “scheduled,” “forecast” and similar expressions are intended to identify forward-looking statements.

The forward-looking statements contained in this press release speak only as of the date of its issuance. Except where required by applicable law, the Company expressly disclaims a duty to provide updates to forward-looking statements after the date of this press release to reflect subsequent events, changed circumstances, changes in expectations, or the estimates and assumptions associated with them. The forward-looking statements in this press release are intended to be subject to the safe harbor protection provided by the federal securities laws.

# # #

Contact:

Bethany Lai, Investor Relations and Communications

[email protected]

Disclaimer: The above press release comes to you under an arrangement with GlobeNewswire. Mango Bunch takes no editorial responsibility for the same.

Disclaimer: The above press release comes to you under an arrangement with GlobeNewswire. Mango Bunch takes no editorial responsibility for the same.